Market participants are patiently awaiting this afternoon’s “Liberation Day” event at the White House’s Rose Garden, during which President Trump is scheduled to unveil large-scale tariffs on US imports. Anecdotal chit-chat spanning from Wall Street to Washington includes wide-ranging speculation, with some analysts expecting targeted duties while others anticipate a flat levy across most nations. And as we wait for the 4:00 p.m. announcement, trading action has been indecisive even with this morning’s pleasant surprise of stronger-than-expected job growth amidst an upside beat on the less impactful factory order report. Stocks and Treasurys have flipped back and forth from losses to gains, but equity volatility protection, commodity futures and forecast contracts have caught consistent bids throughout the session so far.

Hiring Beats Expectations

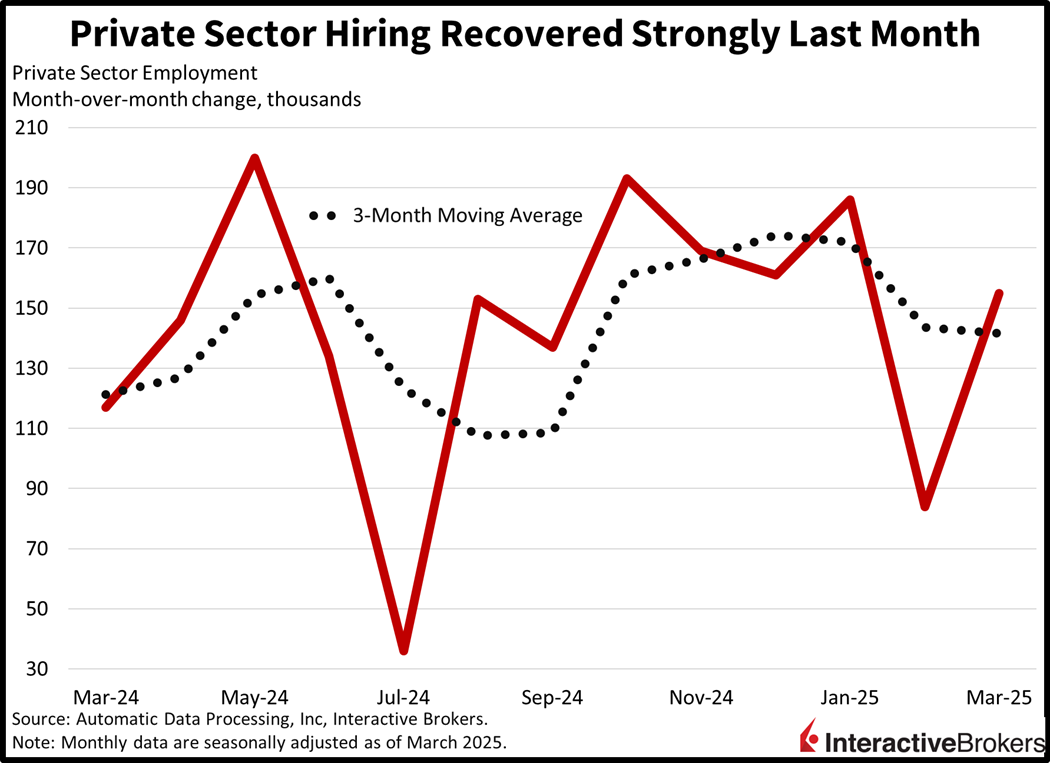

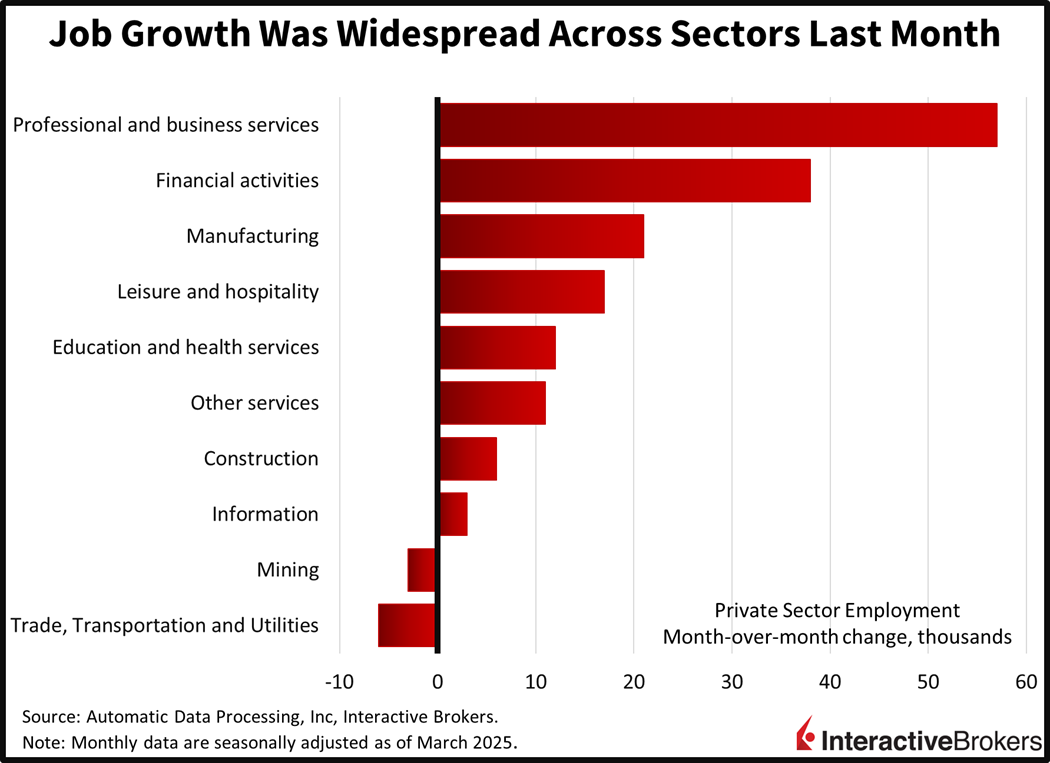

The US private sector ramped up its hiring last month, according to payroll processing company ADP. March job growth of 155,000 eclipsed the 105,000 expectation as well as the 84,000 from February. Employment additions featured a cyclical tilt and were broad-based as the professional/business services, financial activities, manufacturing and leisure/hospitality sectors led with roster gains of 57,000, 38,000, 21,000 and 17,000. Education/health services, other services, construction and information added at more modest degrees of 12,000 or less. Conversely, the trade/transportation/utilities and mining segments lost 6,000 and 3,000 jobs respectively. Labor expansion activity was also firm across business sizes, with small (1-49 employees), medium (50-499) and large (500+) establishments increasing workforces by 52,000, 43,000 and 59,000.

But Wage Pressures Soften

Compensation trends slowed down a bit, however, despite hiring gaining momentum. ADP reported decelerating wage growth across both job changers and job stayers. The median year over year (y/y) change in annual pay was 6.5% and 4.6%, a downtick from February’s 6.8% and 4.7%. The 1.9% gap matches the lowest spread on record since last September, indicating less of an incentive for workers to switch employers, signaling softening labor conditions. The data series began in December 2020.

Factory Orders Ease

Factory orders slowed in February but managed to surpass the median economist expectation. Purchases rose 0.6% m/m following a 1.8% increase in January, beating projections by a tenth of a percent. Transportation equipment drove the gain amidst greater demand for defense aircraft and automobiles, which were up 9.2% and 1.9% during the period. Furthermore, durable products outperformed nondurables, advancing 1% m/m versus 0.3%.

Equities Climb After Moving Sidewise

Stocks turned decisively higher ahead of this afternoon’s announcements while interest rates crept up in volatile trading. All major equity benchmarks are now in the green, with the Russell 2000, Nasdaq 100, S&P 500 and Dow Jones Industrial indices climbing 0.8%, 0.4%, 0.4% and 0.4%. Every sector is positive except for energy, which is near its flatline. Leading the bulls are consumer discretionary, utilities and financials; they’re advancing by 0.9%, 0.7% and 0.6%. Treasurys and the greenback are taking losses, with the 2- and 10-year maturities seeing their yields rise 2 basis points (bps) while they change hands at 3.90% and 4.18%. The Dollar Index is lower by 35 bps as the US currency depreciates against most of its counterparts, including the euro, pound sterling, franc, yuan and Aussie tender. It is appreciating relative to the yen and loonie, however. Commodities are bullish across the board with crude oil, silver, gold, lumber and copper increasing 0.6%, 0.6%, 0.5%, 0.3% and 0.2%. WTI crude is at $71.50 per barrel despite a large stateside inventory build, as potential trade restrictions, tightened sanctions and tariffs weigh on global supply prospects.

Tariff Announcement Likely to be Pivotal

In conclusion, this afternoon’s events are unpredictable, but markets are expecting a binary outcome heading into the announcements. A lighter-than-feared message of targeted and not blanket tariffs would likely send stocks north tomorrow. But a negative response to punitive duties across the board can spark volatility, causing equities to decline further. Similarly, short-term economic performance will benefit from trade collaboration and not confrontation, but this Administration has communicated its commitment to the long haul amidst its goals of bringing back the good ole days of stateside manufacturing dominance.

International Roundup

Singapore Manufacturing Slows as Trade Fears Grow

Singapore’s manufacturing sector slowdown continued in March with the sectors’ Purchasing Managers Index (PMI) dropping from 50.7 in the preceding month to 50.6, according to the Singapore Institute of Purchasing and Materials Management. Results above 50 imply expansion and readings below that level depict contraction. It is the lowest reading in eight months. Separately, the electronics PMI dropped from 51 to 50.9. The broader PMI decline is consistent with most other Asian nations that are experiencing slowing factory activities and is believed to be driven, in part, by trade conflict concerns and economic uncertainty.

Education Leads South Korea Cost Pressures

South Korea’s Consumer Price Index climbed 0.2% m/m last month, matching expectations and easing slightly from 0.3% in February. On a y/y basis, the gauge climbed 2.1%, slighter hotter than expectations for an unchanged 2%. Excluding food and energy, the CPI rose 0.2% m/m and 1.9% y/y. Within the broad index, education experienced the strongest cost pressure with a 1% m/m jump followed by 0.4% hikes for both the food and non-alcoholic beverages category and the restaurants and hotels classification.

Reforms Needed to Address Australia Building

Australia building approvals declined 0.3% m/m in February, according to the Australian Bureau of Statistics. While the result was much worse than the 6.9% expansion in the first month of the year, it surpassed the 1.4% contraction anticipated by economists. On a y/y basis, approvals climbed 9.1% compared to 9.4% in January. Approvals for private residential construction climbed 1% compared to 1.4% in January but when excluding houses, permits declined 1.5%.

Aussie Manufacturing and Industry Weaken

The Australian Industry Group (AIG) Manufacturing Index fell from -8.2 in February to -29.7 in March, with the negative results depicting continued contraction. The organization’s Industrial gauge also weakened, descending 3.1 points to -22.2. Within the industry category, the sales component sank to -31.5 but the job market gauge climbed 5.8 points to -7.3. Survey respondents said new orders and demand kept declining in March, in part due to the country’s election uncertainty and brush fires.

Disclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!