Wisdom of AI")

A few days a year, I’m envious of bond traders. It’s not that I find their lives inherently more interesting, it’s that they get more holidays than those of us who focus on equities. One of them was yesterday, when they were closed for Veterans Day.[i] Now that they’ve returned, they appear to have an unpleasant message for markets.

One of the “Trump trades” involved expectations of higher yields. Bond investors are understandably nervous about the potential budgetary and inflationary implications of tariffs and deportations. Either has the potential to raise prices and/or cost money depending upon whether and how they are implemented. We saw yields shoot higher last week as traders processed the incoming election returns, but then saw them recover most of their losses over the remainder of the week. A solid 30-year auction and a generally benign FOMC meeting certainly helped calm bonds’ jitters.

Unfortunately, after yesterday’s hiatus, those jitters returned today. We now have 2-year yields at 4.32%, above their post-election worst and about 15 basis points above their pre-election level. 10-year yields are higher by a similar amount, though at 4.41% they have not topped Wednesday’s 4.47% peak.

6-Day Line Chart, 2-Year Treasury Yields (white), 10-Year Treasury Yields (blue)

Source: Bloomberg

We see the Treasury yield curve with a generally parallel shift higher for notes with longer than 1 year to maturity.

US Treasury Yield Curve, Today (green), 1 Week Ago (yellow)

Source: Bloomberg

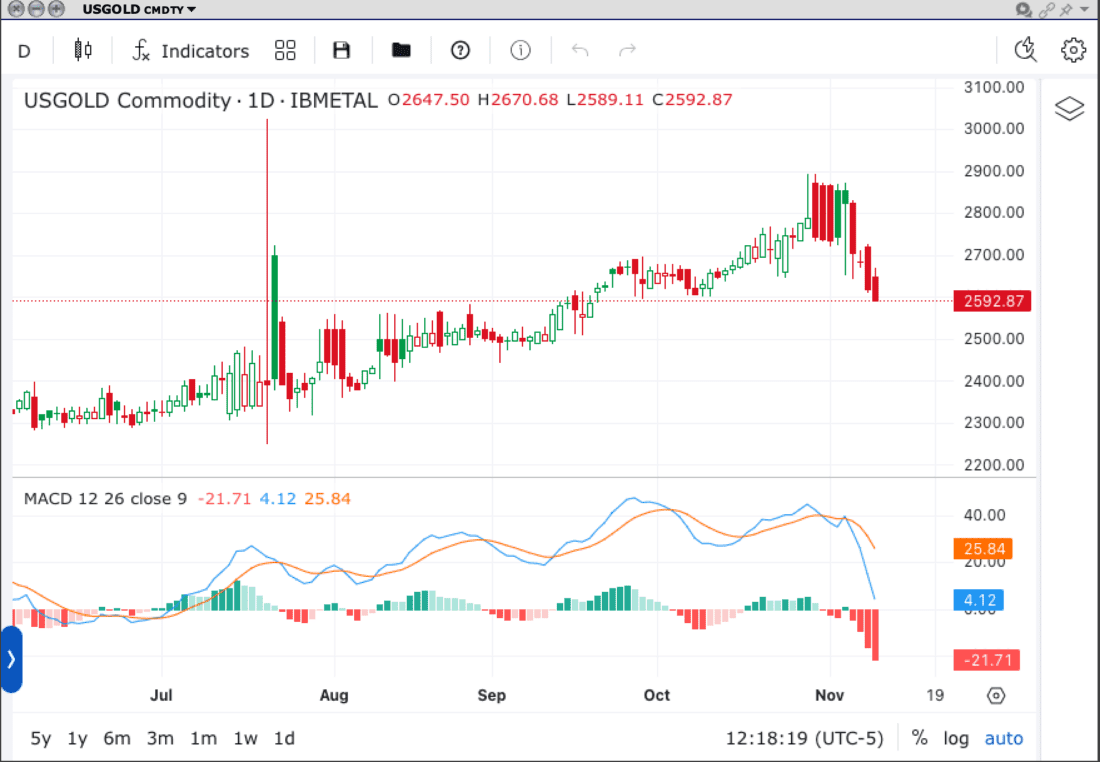

Higher yields are also affecting currency markets. Higher US yields tend to make the dollar more attractive against foreign currencies, and we see the greenback at multi-month, or longer, highs against the Euro, Yen, Canadian dollar, and more. Gold, which often acts like an “anti-dollar” continues to fade from recent highs amidst dollar strength. (Though it could of be suffering as traders pile into cryptocurrencies instead).

Spot Gold, 6-Months, Daily Candles (top), with MACD (12,26,9, bottom)

Source: Interactive Brokers

Although stocks have succumbed to some profit-taking this morning, we can’t necessarily blame it on the bond market today. Higher yields certainly aren’t helpful for stocks but remember that stocks had essentially sideways moves for the prior two sessions. It is not unusual for stocks to have difficulty piercing major psychological levels, like 6,000 for the S&P 500, nor is it odd that we might see some consolidation or profit-taking after last week’s sharp advance.

But over time, higher yields and a stronger dollar are not conducive to higher stock prices. When fundamental valuations matter – and it’s not clear to me that they do matter to many investors right now – higher rates decrease the present value of a company’s future earnings and cash flows. That should reduce the amount that investors are willing to pay. Furthermore, a stronger dollar is not helpful for US multinational companies because it reduces the value of any sales made in foreign currencies. This becomes a question of timing, though. It might matter today, tomorrow, weeks from now, or seemingly never. The better the market psychology, the longer that stocks can withstand higher yields. And market psychology is undoubtedly quite robust.

With one day back from a long weekend and only a week since the election, it is far too soon to say whether the so-called “bond vigilantes” are the ones pushing rates higher. But they bear watching (no pun intended, maybe). If enough investors, domestic or foreign, become sufficiently concerned about the path of fiscal policy in the incoming administration, that could provide a headwind which might offset the gusty tailwind that pushed stocks higher after the election.

—

[i] Bonds were also closed for Columbus Day on October 14th. And it’s even more infuriating when they close early ahead of long weekends, such as 2pm on the Friday before Memorial Day. Goodness knows, bond traders can’t be required to sit in traffic like the rest of us working stiffs. The only small consolation is that on half-days, such as the Friday after Thanksgiving, bonds are open for one hour longer than stocks.

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.

Leave a Reply

Disclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Is it possible to buy individual stocks on the Swiss exchange thru interactive brokers?

Yes

Thank you for reaching out. Yes, it is possible to buy stocks on the Swiss exchange at IBKR. You can view our available Products and Exchanges on our webpage: https://spr.ly/IBKR_ProductsExchangesCampus

Why is there suddenly a ‘concern’ over the path of fiscal policy? What was or is the existing one and no concerns over that??? And not to split more hairs but how has the FOMC meeting been ‘benign?’ As far as what the Fed will do, well perhaps it was; but the storm created when Powell got his ‘back’ up over his resignation has persisted thru today. The question that should be asked now is not whether he stays but what a fight, legal or otherwise, meaning thru the media, will do to the financial system/markets, etc?

Read the article… “One of the “Trump trades” involved expectations of higher yields. Bond investors are understandably nervous about the potential budgetary and inflationary implications of tariffs and deportations. Either has the potential to raise prices and/or cost money depending upon whether and how they are implemented.”

This writer of this article is speaking on behalf of the bond traders, in other words, putting words in their mouths without their input. Bond traders are not nervous about the “potential budgetary and inflationary implications of tariffs”. Removing the freeloaders will save a great deal of money for city, county, state and federal governments. Additionally, bond traders understand that inflation is caused by the expansion of the money supply. Not long ago, you could buy a new car for $5000. Tariffs are NOT responsible for the price of new cars today. The convern voiced in this ultra biased article is strictly from a demonrat viewpoint. It is NOT the viewpoint of bond traders.

A fight will end with No Winners. Bonds, Gold & The Crypto charge is fundamentally Creating Dazed, Dyslexian, Dystopian and Confusing, ( WHAT IF? < This & That ) happens. Confusion creates ambiguity . Therefore, a 6.25% to 12.5% ( less likely than 6.25%…) sell off is a disturbing highly distinct possibility.

Hello Sir, this is out of topics. Although you are right about the market. Can you do something about my situation. Please let me reopen an Interactive broker account with IB Canada. I am a big fan of yours and TWS. The greatest platform ever created to me. I worked hard to learn TWS for 2 years. But I then became a legal representative and could not trade for a wild. Did not feel like doing it. But I did use the paper account from time to time along a monthly data subscription. My account was suddenly shut down because I would not trade live. As a canadian, we don’t have other alternative for futures trading. Nothing comparable commissions wise and Forex wise. I maybe wrong here but only Mr Peterffy would use dazed, dystopian dyslexian terminology. Anyway If I am I apologyse for this weird reply and if I am right I don’t apologize for wanting to be a IB client again.

Thank you for reaching out. Please view this FAQ for instructions to reopen a closed account: https://www.interactivebrokers.com/faq?id=28238991

We hope this helps!