Wisdom of AI")

The bull run is continuing in markets as investors gear up for Fed Chief Powell’s second day of congressional testimony as well as a heavy week of Treasury issuance and inflation data. This afternoon features a $39 billion 10-year note offering, while tomorrow’s events will include the June CPI as well a 30-year bond auction totaling $22 billion. Investors are eagerly awaiting the first read on last month’s price pressures, which may strengthen the odds of a September rate reduction; they are already lofty at 72%.

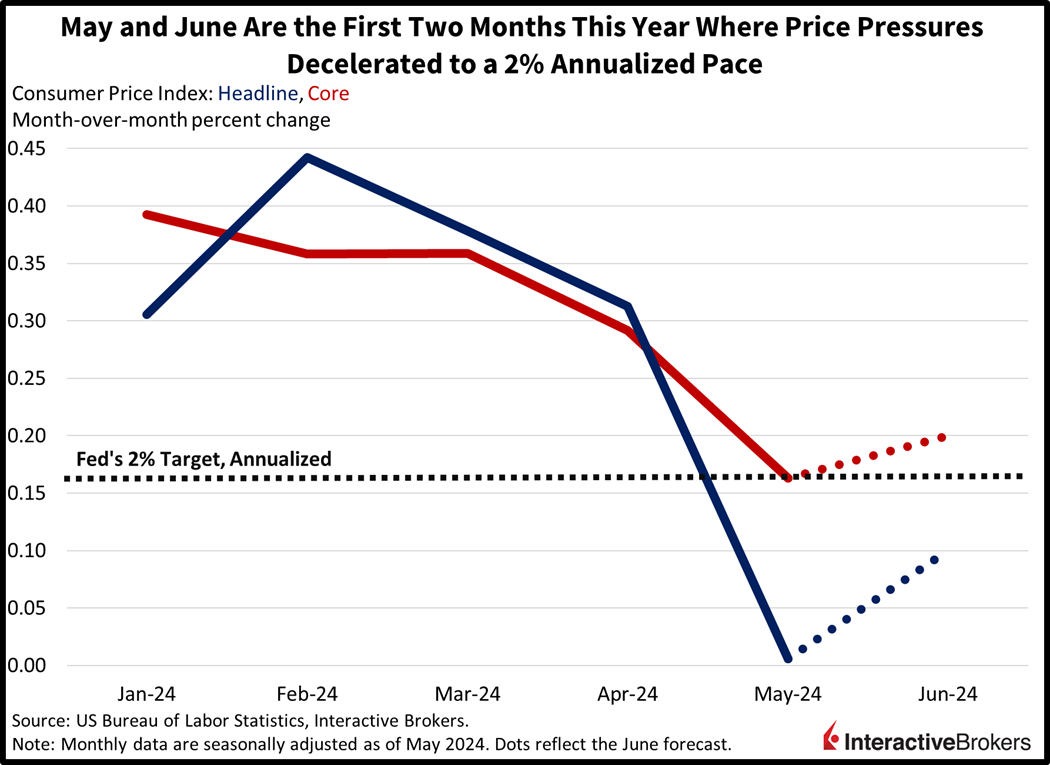

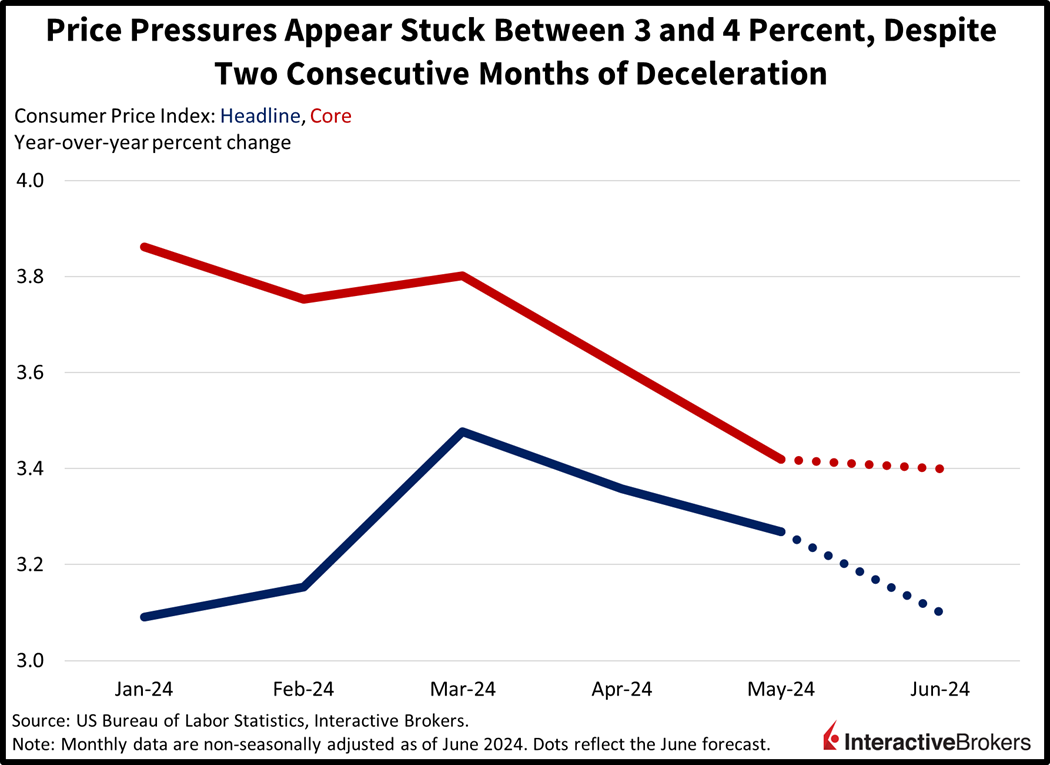

Inflation Is Batting .333 in 2024

While an average of .333 is terrific for a third baseman or a right fielder, it’s particularly awful in basketball for a small forward or point guard’s field goal percentage. That’s the score for inflation data coming in favorably, or the past two out of six months. Is the Federal Reserve swinging bats or shooting hoops? I’m pretty sure it’s the latter, but only time will tell.

Tomorrow’s Consumer Price Index (CPI) is likely to offer the second report of the year when price pressures arrive in the Fed’s 2% ballpark on an annualized, month-over-month (m/m) basis. Indeed, inflation reports from January to April weren’t cooperative, with charges rising well above the 0.167% m/m standard. The June CPI is likely to rise 0.1% m/m and 3.1% year over year (y/y) overall and 0.2% m/m and 3.6% y/y for core. The month’s disinflation will be led by lower costs for energy, new and used automobiles and apparel. On the other hand, charges for shelter, medical care, transportation services and food will likely serve to offset progress. Finally, there’s room for core inflation to beat to the upside and come in at 0.3%, as the effects of all-time high existing home prices and lease renewal increases overwhelm the weaknesses in fresh builds and new rents.

Powell Says Disinflation Is Continuing

During his Congressional testimonies yesterday and this morning, Chairman Powell reiterated past points about the central bank needing more data pointing to sustainable progress in fighting inflation before cutting rates, but he also noted that disinflation has returned after price pressures gained in the later part of 2023. With that in mind, he opined that the most likely path for the Fed is to ease policy, but he refrained from speculating on when the organization will make its initial move. He added that recent data show that the job market is softening and much like prior to the pandemic, the economy is no longer overheated. The Fed is ready to accommodate sooner rather than later if the labor market cools excessively.

Equities Nail Fresh All-Time Highs

Stocks are reaching for further upside while fixed-income and the greenback are in wait-and-see mode. Tomorrow’s CPI will certainly be important, with the potential for a beat on core potentially augmenting our journey across the monetary policy bridge. July m/m price pressures are already tracking at 0.27% on headline and 0.31% on core, which means there’s room for disappointment as we approach the September Fed meeting. For today, though, all major US equity indices are higher, being led by the Nasdaq Composite, (what else is new?). It’s up 0.5%. The S&P 500, Russell 200 and Dow Jones Industrial benchmarks are gaining at more modest rates of 0.3%, 0.3% and 0.2%. Sectoral breadth is positive with every segment pointing north except for the financials group, which is unchanged. The bull charge is being piloted by materials, technology and energy, which are up 0.8%, 0.6% and 0.5%. Treasurys and the greenback are little changed, with the 2-and 10-year maturities changing hands at 4.63% and 4.3% while the Dollar Index trades at 105.03. The US currency is appreciating against the yen, franc and yuan but depreciating relative to the euro, pound sterling and Aussie and Canadian dollars. Commodities are mostly loftier, with copper, gold, crude oil and silver higher by 1.2%, 0.7%, 0.7% and 0.6%. Lumber is down 0.3%, meanwhile, reaching a fresh year-to-date low as the real estate recovery has been derailed by a steepening yield curve. WTI crude oil is trading at $82.33 per barrel after OPEC + upwardly adjusted its forecast for global economic growth to 2.9% and the US reported an inventory draw last week.

The Gulf Between Earnings and the Economy Widens

As investors sift through Powell’s recent comments, a dichotomy between growing earnings expectations and weakening economic prints is widening. Indeed, the move from forward earnings of $250 on the S&P 500 to $259 has occurred as activity data have surprised to the downside in aggregate. Many economists are sharpening their pencils and raising the odds of a downturn in the third quarter of this year on the back of overwhelmed consumers that are battling the pressures of elevated rates, tall prices and reduced credit availability. Strategists, meanwhile, are pointing to a much brighter picture of an artificial intelligence revolution that will drive productivity growth and revenue progress. Occurring simultaneously has been a year-to-date move north in interest rates alongside a violent expansion in earnings multiples. This earnings season may reconcile the discrepancy between cautious economists and exuberant strategists.

Visit Traders’ Academy to Learn More About the Consumer Price Index and Other Economic Indicators

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.

Leave a Reply

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Powell must be playing politics with a rate cut as financial markets continue to hit daily highs.

Thanks

Thanks for engaging, Willie!

The problem with all of this is everything is based on what “could be” rather than what is. Looking forward is inherently risky, which causes all of the so-called “excitement” in the stock market when it goes up, and the so-called “fear” when it drops. There needs to be a better way. Now that AI is approaching quickly, I am sure there are already many unscrupulous characters around the world wanting to be the first to “develop” a fail-safe stock market prediction software. The trouble with this is that it will make the stock market even more volatile in the long run. This is not about investing anymore; it is about blind greed from a few individuals and companies that don’t care at all about fundamentals. We are seeing this already with the so-called “meme” stocks and the crypto currencies mania. Everything hinges on the “next thing” to just keep the economy above water, so to speak, but no real efforts are made to stabilize markets and provide real long-term investments that benefit the majority of the population. Capitalism as a way of economic growth is flawed, and only when there is a move towards an economy that encompasses greater sharing of wealth will there be long-term prosperity for all.

Yup. Playing politics with the stock market it seems. I’m in!