")

Versus Equity Analysts")

The third quarter start has investors worried that stocks may have run too hard too fast, as market participants hesitate to add risk to their portfolios. Rates continue rising in bear-steepening fashion, meanwhile, as global appetites for central bank rate reductions contend with inflationary concerns at the long-end. Price pressure anxiety in the present is stemming from heightening geopolitical tensions, dismal fiscal outlooks and uncertain election trends. Wall Street is also gearing up to hear from Fed Chief Powell, who will provide clues tomorrow morning regarding the number of steps remaining on the cloudy and perilous journey across the monetary policy bridge.

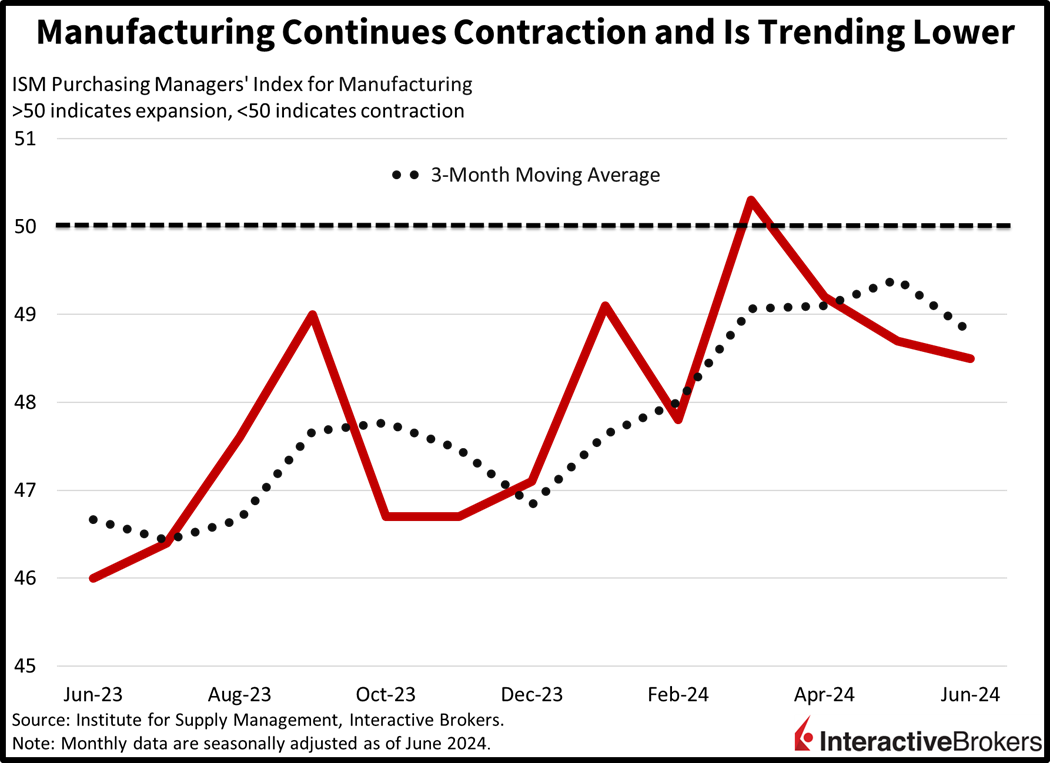

Manufacturing Remains in Contraction

A popular gauge of US manufacturing conditions that correlates positively with corporate earnings expectations posted yet another weak release this morning. June’s Purchasing Managers’ Index from the Institute for Supply Management (ISM) printed the 19th contraction in the last 20 months, arriving at a score of 48.5 and missing the median estimate of 49.1. Additionally, the figure reflected a deeper rate of decline than May’s 48.7. Weighing on performance were sluggish consumer demand and a lack of capital expenditure plans with the following components scoring the noted results that missed the contraction-expansion threshold of 50:

- Backlogs, 41.7

- Inventories, 45.4

- Production, 48.5

- Employment, 49.3

- New orders, 49.3

Costs didn’t cooperate with weakening conditions though, as the prices paid component decelerated to just 52.1, remaining firmly in growth territory.

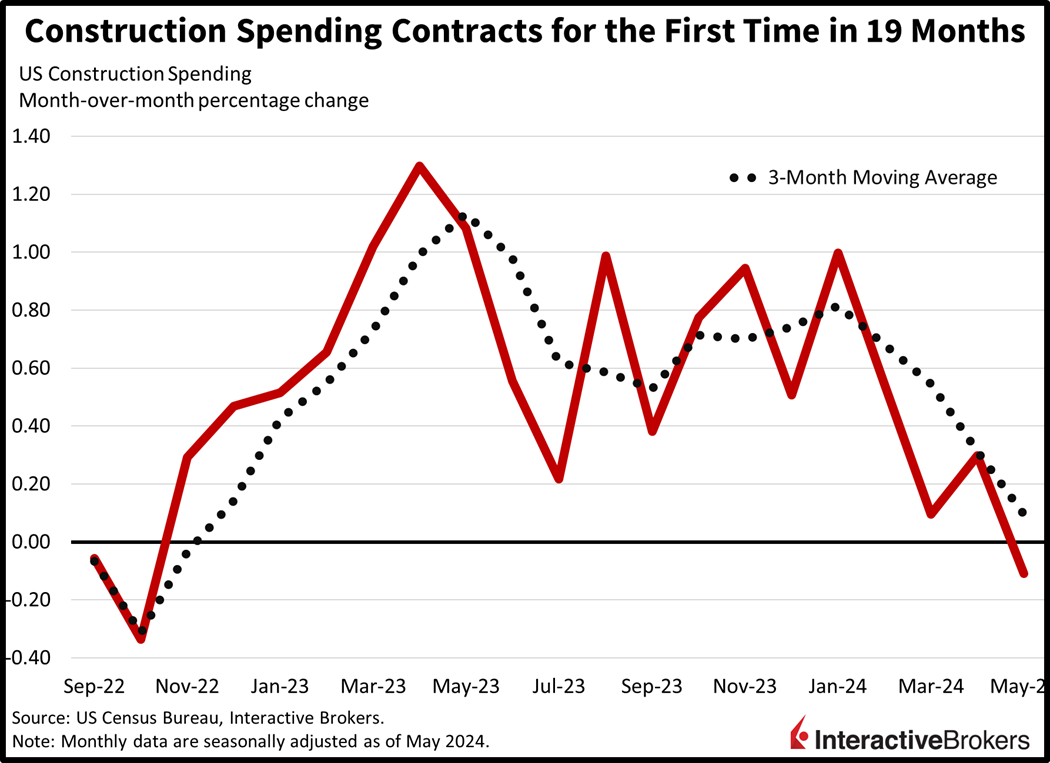

Construction Outlays Shrank for the First Month in 19

Another indicator of real estate activity contracted sharply as elevated mortgage rates and stubborn valuations continue to hamper affordability. May construction spending shrank 0.1% month over month (m/m) despite analysts anticipating growth of 0.1%. In comparison, April featured a m/m growth rate of 0.3%. The residential category, which comprises about half of the report, declined 0.2% m/m, with the single-family segment slipping 0.7% while multi-family was unchanged. The religious, health care and office property types also weighed on results, falling 2.9%, 1.4% and 1.3% during the period. Offsetting some of the weakness, however, were the sewage, manufacturing and transportation components, which grew 2.2%, 1.3% and 0.9% m/m. Recently, pending home sales hit an all-time low, home building sentiment sank and the number of building permits and housing starts also contracted.

French Political Fears Ease

French markets launched a relief rally this morning after neither the far-right Marine Le Pen National Rally or the left-wing New Popular party achieved a commanding majority during the initial round of snap parliamentary elections, but political uncertainty could potentially drive volatility. Investors feared that either party would weaken efforts by President Emmanuel Macron’s centrist coalition government to reduce the country’s deficit, which is projected to be 5.3% of gross domestic product, exceeding the European Union’s 3% limit. The National Rally secured 33.2% of the vote while the New Popular Front won 28% and Macron’s coalition captured 20.8%. Investors are now looking toward the second round of voting on July 7, which consists of only candidates who received at least 12.5% of ballots in the initial voting. It’s likely that France will end up with a hung parliament, relieving fears of concentrated power. The CAC 40 stock index of French equities jumped 2.8% in early trading, but then retreated slightly with only a 1.7% gain as trading progressed. The yield spread of French bonds over German bonds, which has been elevated due to political uncertainty, narrowed approximately 7 basis points (bps).

Political Fears Energize Bears

Markets are bearishly tilted as turbulent political conditions have unanchored inflation expectations. A foggy governmental landscape and heightening geopolitical worries are sending yields, the greenback and commodities north while stocks waver amidst the pressure of loftier costs of capital and taller uncertainty. Major equity indices are mixed against the backdrop, however, with the Russell 2000 and S&P 500 down 1.1% and 0.1% while the Nasdaq Composite and Dow Jones Industrial benchmarks are 0.2% and 0.1% higher. Sectoral participation is negative, though, with just four out of eleven segments in the green. The consumer discretionary, financials and energy components are leading the charge to the upside with the baskets positive by 0.2%, 0.2% and 0.1%. But the pain to the downside is much fiercer, with real estate, materials and industrials shedding 1.4%, 1.4% and 1%. Amidst the action, market players are staying away from Treasurys, with the 2- and 10-year maturities changing hands at 4.78% and 4.48%, 2 and 8 bps higher this session due to harsher Fed easing projections and rising uncertainties. The greenback is gaining for the same reasons, with the dollar up relative to most of its major peers including the pound sterling, franc, yen, yuan and Aussie and Canadian dollars. The US currency is losing versus the euro though. Commodity action is bullish as crude oil, copper, silver and gold gain 1.6%, 0.8%, 0.4% and 0.1%. Lumber is down 2.2%, however, as folks don’t happen to see the light at the end of the real estate tunnel. WTI crude is trading at $82.80 per barrel, its highest level since April as investors price in a geopolitical war premium to protect against potential supply disruptions on the back of heating hostilities between Beirut and Jerusalem.

A Hawkish Powell Could Ignite Volatility

Markets and the economy face a tightly coiled spring of risks that could release and spark volatility this week, especially if Fed Chair Powell provides a hawkish message tomorrow at the European Central Bank Forum in Sintra, Portugal. Meanwhile, during last week’s presidential debate, neither candidate proposed policies that would reduce the country’s fiscal deficit, which is quickly growing to an unsustainable level. Meanwhile, the US political landscape is highly uncertain as members of the media and various Democrats call for President Joe Biden to step down from the race for the White House following his weak debate performance. Geopolitical risks are also significant, with Israel increasing its military actions against Hezbollah in Lebanon, Houthi rebels continuing to attack ships in the Red Sea to support Iran, fears of a Chinese invasion of Taiwan growing and the Ukraine-Russia war showing no sign of easing. Regarding global fiscal policy, France’s political battle is emblematic of the growing threat of excess sovereign debt and high inflation, with the Bank for International Settlements urging central banks to hike interest rates and move away from using debt to generate short-term economic growth.

Visit Traders’ Academy to Learn More About ISM-Manufacturing and Other Economic Indicators

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.