- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted October 20, 2023 at 11:15 am

While the US economy has been resilient this year, the lagged effects of tightening are likely still to come.

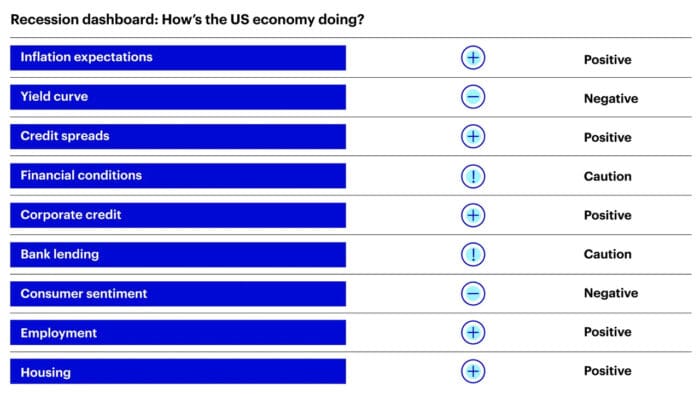

Inflation expectations, credit spreads, corporate credit, employment, and housing aren’t in recession territory.

The yield curve, financial conditions, bank lending, and consumer sentiment are showing recession signs.

There’s been talk of a recession in the US economy for more than a year. Although one hasn’t materialized yet, it’s important to remember that the economic impact of interest rate tightening by the Federal Reserve has historically lagged rate hikes by 12 to 18 months.1 That’s why, in our view, a mild recession may be on the horizon. We also believe that last year, the stock market likely priced one in. I keep a close watch on several economic indicators that typically signal a recession. Here’s a quick summary of the current state. Most indicators are positive and do not signal a recession. Some are negative, and for some, the status is cautious because they’re showing signs of declining.

Heightened inflation expectations hasten monetary policy tightening cycles, which in turn hasten the end of business cycles. Plain and simple. Inflation in 2022 was well above the Fed’s “comfort zone,” resulting in a series of interest rate hikes. The good news: Inflation expectations have fallen considerably based on the inflation breakeven, a measure of expectations of the future direction of inflation. This suggests the end of policy tightening is likely near.2

Recessions typically play out in four steps. We’re in step three right now.3

1. Fed initiates a tightening cycle

2. Spread between 10-year US Treasury rate and 2-year US Treasury rate inverts

3. Spread between 10-year US Treasury rate and 3-month US Treasury rate inverts

4. Recession commences within 1 to 2 years

Credit markets are often viewed as a “canary in the coal mine,” providing an early signal that conditions in the economy are weakening meaningfully. Credit spreads, using the options-adjusted spread on the Bloomberg US Corporate High Yield Bond Index, have widened modestly as monetary policy tightened but remain below levels that have preceded past recessions.4 It’s likely a testament to the current fundamental strength of US businesses.

Financial conditions have tightened meaningfully, driven by higher real interest rates and a stronger US dollar against major trading partners (for example, the euro, the Japanese yen, and the Chinese yuan). Leading economic indicators such as the Institute for Supply Management Manufacturing Purchasing Managers’ Index (Manufacturing PMI) is in contractionary territory (below 50) but may be bottoming.5 Critical question: Will easing financial conditions lead to additional interest rate hikes and further pressure on the US economy?

The fundamentals of the economy remain sound. Typically, a meaningful growth in corporate credit precedes a recession. That doesn’t appear to be the case today.6

Banks are tightening lending standards, which is often the case before recessions. Bankers tend to become more concerned about creditors as growth slows. More than half of the bankers surveyed in the Federal Reserve Senior Loan Officer Survey are reporting tighter lending standards to large- and medium-sized businesses.7

Consumer sentiment had declined meaningfully, driven by higher gas and food prices and elevated costs across much of the consumer goods and services in the Consumer Price Index (CPI). (Recent moderating inflation, however, could be the silver lining.) The consumer has been remarkably resilient to date, and sentiment has picked up recently, according to the University of Michigan Sentiment Index.8 This warrants watching because the consumer is the backbone of the US economy.

The job market is strong. The unemployment rate is currently 3.8%.9 Will that continue? Can the Fed restore inflation to a more reasonable level without increasing the unemployment rate?

The number of authorized housing units tends to decline ahead of a recession, which may be beginning to happen. New privately owned housing units authorized but not started have been declining since the beginning of the year, according to the US Census Bureau.10

While most of the economic indicators I watch aren’t signaling a recession, some are negative and some warrant caution. Based on the lagged effects of tightening, however, we believe the US may experience a mild recession in early 2024.

Footnotes

—

Originally Posted October 18, 2023

Is a US recession coming? by Invesco US

Important information

NA3163770

Investors should consult a financial professional before making any investment decisions. This does not constitute a recommendation of any investment strategy or product for a particular investor.

All investing involves risk, including the risk of loss.

Past performance does not guarantee future results.

Investments cannot be made directly in an index.

M2 is a measure of the money supply that includes cash and checking deposits as well as savings deposits, money market securities, mutual funds, and other time deposits.

The Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services. Core CPI is the same measure but with food and energy goods and services removed from the basket.

The opinions referenced above are those of the author as of Oct. 12, 2023. These comments should not be construed as recommendations but as an illustration of broader themes. Forward-looking statements are not guarantees of future results. They involve risks, uncertainties, and assumptions; there can be no assurance that actual results will not differ materially from expectations.

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial advisor/financial consultant before making any investment decisions. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

NOT FDIC INSURED

MAY LOSE VALUE

NO BANK GUARANTEE

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s Retail Products and Collective Trust Funds. Institutional Separate Accounts and Separately Managed Accounts are offered by affiliated investment advisers, which provide investment advisory services and do not sell securities. These firms, like Invesco Distributors, Inc., are indirect, wholly owned subsidiaries of Invesco Ltd.

©2024 Invesco Ltd. All rights reserved.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Invesco US and is being posted with its permission. The views expressed in this material are solely those of the author and/or Invesco US and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!