Wisdom of AI")

The post “Stock Market Valuation and Impact of Inflation” first appeared on Light Finance Blog.

If 2022 has taught us anything, it is that our understanding of the inflationary process is woefully incomplete. Increasingly, it seems that the easy money era of the 2010’s created a blind spot in the market: stable inflation and ample liquidity were taken for granted. The risk of high (indeed, very high) inflation was deeply discounted which resulted in a significant misallocation of investor capital.

In some ways, this is understandable. Inflation had been in a steady decline for decades and in the most recent one routinely surprised to the downside. Prudence and a healthy appreciation for inflation consistently went unrewarded and was often disrespected. It was against this backdrop that investors were confronted with the most significant fiscal and monetary intervention since WWII, an epic dislocation in supply chains and war that has strangled critical commodities.

The objective of this post to provide an analysis of inflation and market valuation. We’ll find that impact of inflation on the market is highly nonlinear, but that a reasonably tight relationship exists when inflation is at extremes.

A Puzzlingly Close Relationship

Stock prices reflect the expected value of future cash flows (think we all agree on this one!). It follows that low earnings yields (i.e., high PE Ratios) reflect some combination of low discount rates and/or high expected future earnings growth. This is essentially the story of the “disruptive tech” stocks that have been ubiquitous during the easy money era. However, various growth metrics are only weakly correlated with earnings yield fluctuations. Moreover, PE ratios have essentially no ability to predict future earnings growth . These were the classic conclusions of Shiller 2001. Indeed, analysis suggests that earnings yields are more closely associated with inflation than with real yields, nominal yields or other traditional growth metrics.

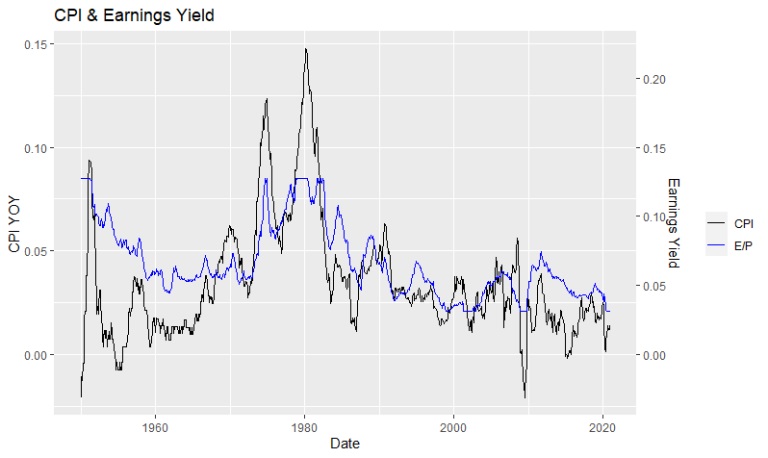

The charts and correlation matrix below hint at this relationship. The first chart depicts the year-over-year change in CPI (LHS) and the TTM earnings-price ratio (i.e., earnings yield) (RHS). While the correlation is not perfect, there is clearly a relationship: high/low inflation is associated with high/low earnings yield.

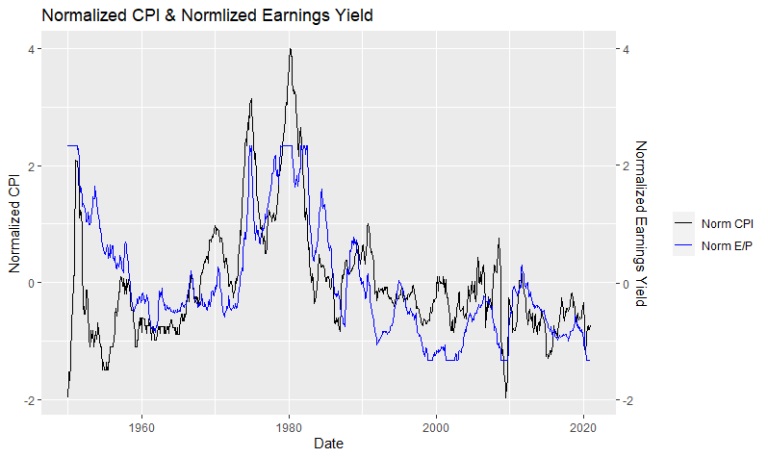

The second plot takes a slightly different view. Here I depict the normalized YoY CPI and normalized E/P ratio to give a sense of the relative relationship. The correlation is quite tight in the first half of the series and particularly so during the inflationary 1970’s and early 80’s, but has been less reliable over the past twenty years.

Source: https://lightfinance.blog/about-aric-lux/, Light Finance.

Data from Online Data – Robert Shiller.

Calculations and charts: Aric Light.

Source: https://lightfinance.blog/about-aric-lux/, Light Finance.

Data from Online Data – Robert Shiller.

Calculations and charts: Aric Light.

Source: https://lightfinance.blog/about-aric-lux/, Light Finance.

Data from Online Data – Robert Shiller.

Calculations and charts: Aric Light.

This relationship may seem surprising because earnings yield is supposed to be a real variable. The textbook explanation is that stocks are real assets. Higher levels of inflation should be reflected in higher nominal earnings and have a negligible impact on stock prices and valuation. However, this description is not corroborated by the data.

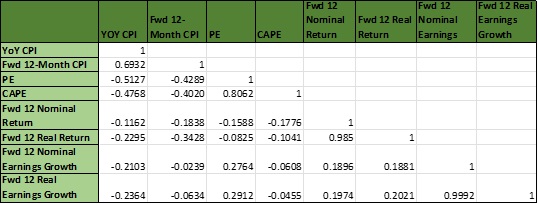

Further examination of the correlation matrix suggests that the connection between valuation and inflation is not easy to disentangle. Valuation appears most strongly negatively correlated with YoY CPI, but also negatively correlated with Next-12 Month CPI. This is suggestive of at least a fairly consistent relationship: high inflation is incorporated into valuation today and, should it persist, also reflected in the future. YoY CPI appears moderately negatively correlated with next-12 months real and nominal earnings growth, but next 12-months CPI is uncorrelated with either. This second observation is harder to reconcile. Finally, both YoY CPI and next 12-months CPI are moderately negatively correlated with next 12-months nominal and real returns. The correlation is stronger for next 12-months CPI particularly where real returns are concerned.

An Underexamined Phenomenon

What are the plausible explanations for this unintuitive association?

- Investors are irrational, risk averse or some combination thereof.

- Real returns may be correlated with expected inflation which leads to a rationally priced inflation risk premium.

- High inflation may impact real earnings growth which is translates directly to lower valuations.

Mogdigliani (1979) investigates the first explanation. Franco (in his eminence) postulates that during inflationary episodes investors commit two major errors when valuing stocks. First, they apply nominal discount rates to real valued cash flows and, second, they fail to incorporate a (sufficiently) higher earnings growth rate into their forecasts. These two errors result in the systematic undervaluation of stocks during periods of high inflation. He suggests that valuing stocks in this way is irrational or reflects a higher level of risk aversion that gets embedded into the discount rate.

In Inflation and the stock market: Understanding the “Fed Model” authors Geert Bekaert and Eric Engstrom make the case that if recessions tend to occur during periods of high inflation, then both equity and bond risk premia will be high at the same time! This would be rational as recessions would translate to lower nominal and real earnings and command a lower multiple. This seems like an appropriate explanation for our current environment of rupturing stock and bond markets. Interestingly, they present evidence across countries and markets which suggests that countries with a higher inflation-recession correlation tend to have a higher correlation between stock and bonds yields which is very reminiscent of the charts in the previous section.

The last explanation is probably the most digestible. A topic hotly debated of late is whether high inflation will result in margin compression. Margin compression is arguably the most intuitive mechanism by which high inflation could result in lower earnings. If firms are unable to pass through higher costs for materials, labor, etc. onto the end consumer or the consumer simply forgoes consumption because prices are too high then it is easy to see how inflation could impact the bottom line. If real earnings are lower, then lower multiples are a natural consequence.

This third explanation will be the focus of the remainder of this post.

The Impact of Inflation on Market Valuation

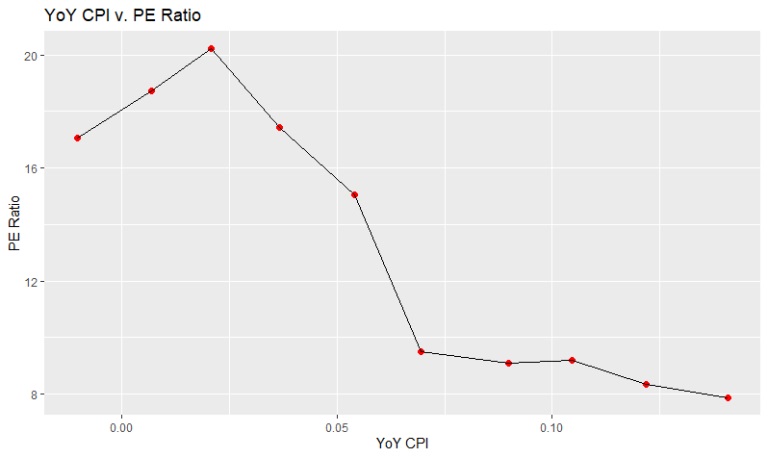

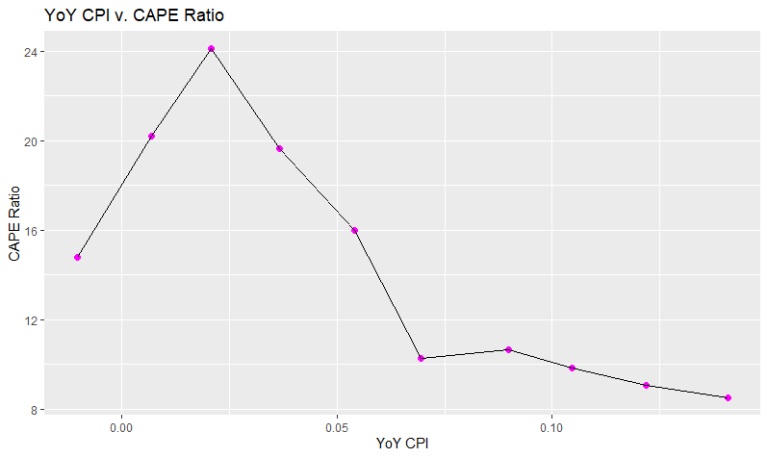

The inflation gauge that I elected to use for this study is CPI. The period under investigation is January 1950 to January 2021. Data comes from Bob Shiller’s website. To study the relationship to valuation I sorted CPI into 10 buckets ranging from a low of -2.09% to a high of 14.76%. I then grouped the relevant variable (CAPE, PE, etc.) for the corresponding month into one of the 10 buckets based on the YoY level of inflation during the month and, finally, computed the average value for each bucket.

(That was a bit of a mouthful, but I think the graphs will make the analysis clear.)

The plots below depict the YoY CPI v. PE and CAPE ratio, respectively. To be clear, the graphs show the average of the valuation ratio (PE and CAPE) in each of the 10 CPI groupings.

Source: https://lightfinance.blog/about-aric-lux/, Light Finance.

Data from Online Data – Robert Shiller.

Calculations and charts: Aric Light.

Source: https://lightfinance.blog/about-aric-lux/, Light Finance.

Data from Online Data – Robert Shiller.

Calculations and charts: Aric Light.

The humped shaped plots suggest a highly nonlinear relationship between inflation and valuation, but several features stand out. The sweet spot for peak valuations appears to occur at positive, but low levels of inflation; right around 2%. Higher levels of inflation are associated with declining multiples, and a valuation cliff appears around the 5% mark. Very high inflation (>6%) is associated with substantially lower multiples, but there doesn’t appear to be a meaningful difference in valuation for inflation of ~6% v. ~14%.

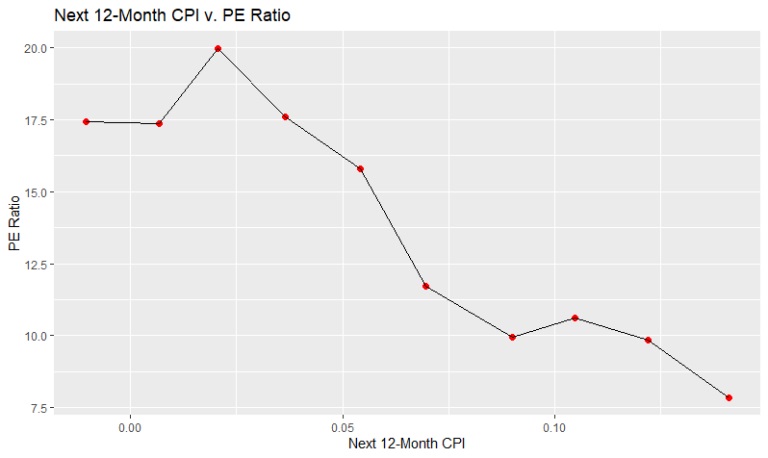

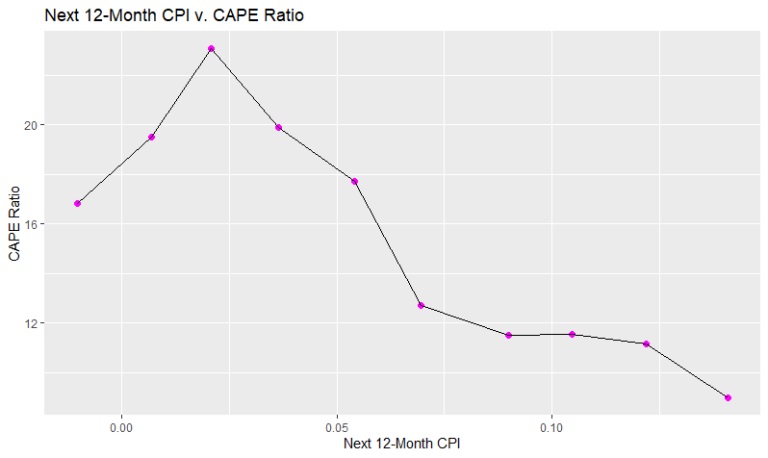

What about forward-looking inflation? It’s one thing if inflation is high today, but it’s quite another for it to remain high in the future. The next two plots depict YoY CPI in the next 12 months v. the PE and CAPE ratio today. The general picture is the same: peak valuations occur at low levels of inflation while low multiples are associated with high inflation. The consistency of these two sets of plots lends some credence to the claim that high inflation is generally bad for stocks.

Source: https://lightfinance.blog/about-aric-lux/, Light Finance.

Data from Online Data – Robert Shiller.

Calculations and charts: Aric Light.

Source: https://lightfinance.blog/about-aric-lux/, Light Finance.

Data from Online Data – Robert Shiller.

Calculations and charts: Aric Light.

Concluding Remarks

In this post we investigated the relationship between inflation and stock market valuation. Inflation is a confusing phenomenon and seldom in history has its process been more confounded than today as we grapple with the effects of supply-chain disruption, pandemic recovery in demand, record money growth and war. Perhaps it should not come as a surprise that inflation’s effect on asset prices is nonlinear. On balance, inflation appears negatively correlated with traditional valuation metrics with severe inflation historically associated with very low multiples. If there is a simple explanation, then perhaps it is that inflation causes unease and uncertainty amongst investors which translates to risk aversion and an unwillingness to pay high premiums for uncertain cash flows.

Hope you have enjoyed this post. Until next time, thanks for reading!

-Aric Lux.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Light Finance and is being posted with its permission. The views expressed in this material are solely those of the author and/or Light Finance and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.